Coinvexity 18

As we settle into the festive period flow has certainly quietened down, a welcome respite given recent events.

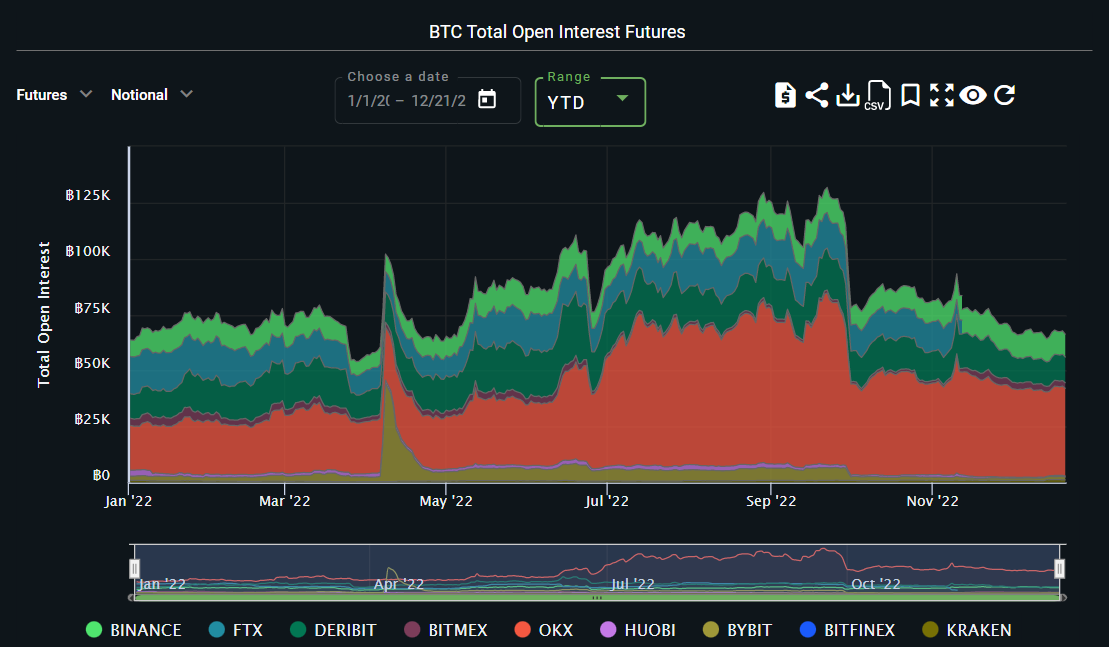

Tackling OI in perps first of all, a gradual but upward sloping trend was visible, this peaked mid-Oct and promptly came off in the ensuing FTX debacle. Any shock seems to have washed out OI since stabilising.

Futures OI remains dominated by OKX at least when considered on a Notional basis. Similarly to perps, OI posted an ongoing increase up until Q3 but since Sep contracts dropped off, OI has struggled to regain prior levels and are back where they began the year. Two things to watch in this space would be the overall trend here i.e. recovery or not? And also, which venue eats up FTX’s share of the market (assuming traders are made whole).

Despite OI in options posting a continued increase in #contracts, the story is rather different from a notional perspective. Gone are the rocket emojis and days of excess as austerity and Wojak settle in as our new bedfellows. Interestingly, Volume still leans heavily towards Call options showing there is a clear bias towards upside exposure both in terms of OI and volume.

Taking a look at BTC vol, following the FTX collapse and FOMC releases (1mo and 1wk respectively) the term structure has resumed normalcy from its prior inverted profile, shifting lower too as the risk washes out.

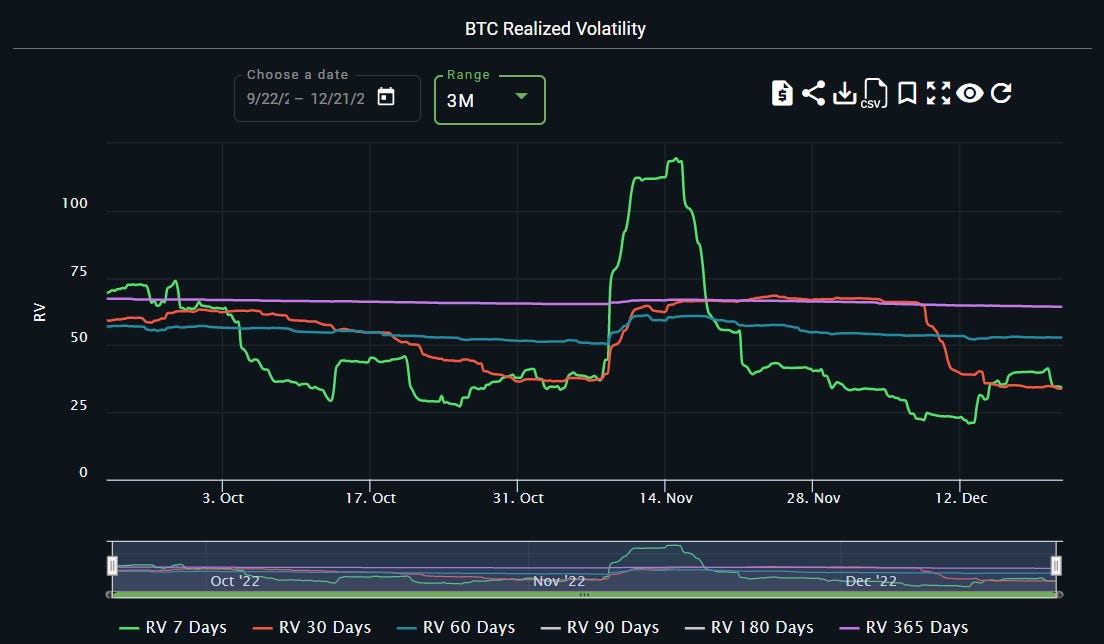

1wk and 1mo Realised vol have shown the most personality here, seemingly reacting to events in the wider market as their dated brethren remain subdued. Looking at 1mo Implieds v Realised, RV keeps pushing lower, presumably in a bid to match levels found in Tradfi. IV, isn’t far behind and prior price action is anything to go by, may well punch lower. 25D Skew shows that much like RV, the near end of the curve remains the most active with 1mo and under posting the greatest signs of life. Interestingly both tenors have converged and reflect the present, strong bias in favour of Puts. The 25D weekly posted levels in excess of 30 vol points.

In ETH the story is not too dissimilar with the term structure reverting from its inverted state and also shifting lower as vol was dampened overall. Realised Vols here are also pushing lower and similarly to BTC, 1mo levels briefly overtook the weekly and still remain entangled. Looking a little deeper into 1mo RV, we can see that it overshadowed all other tenors towards the end of Nov before briskly pushing lower. In an interesting twist, 1yr IV has been overtaken by RV. This inversion of normalcy is reflected by the spread which remains negative after briefly crossing into positive territory halfway through the year.

Looking at the 25d skew in ETH the bias clearly reflects the overarching bear market with 1wk and 1mo peaking around 25 vol. 1wk prices have receded closer to parity but 1mo remains relatively elevated.

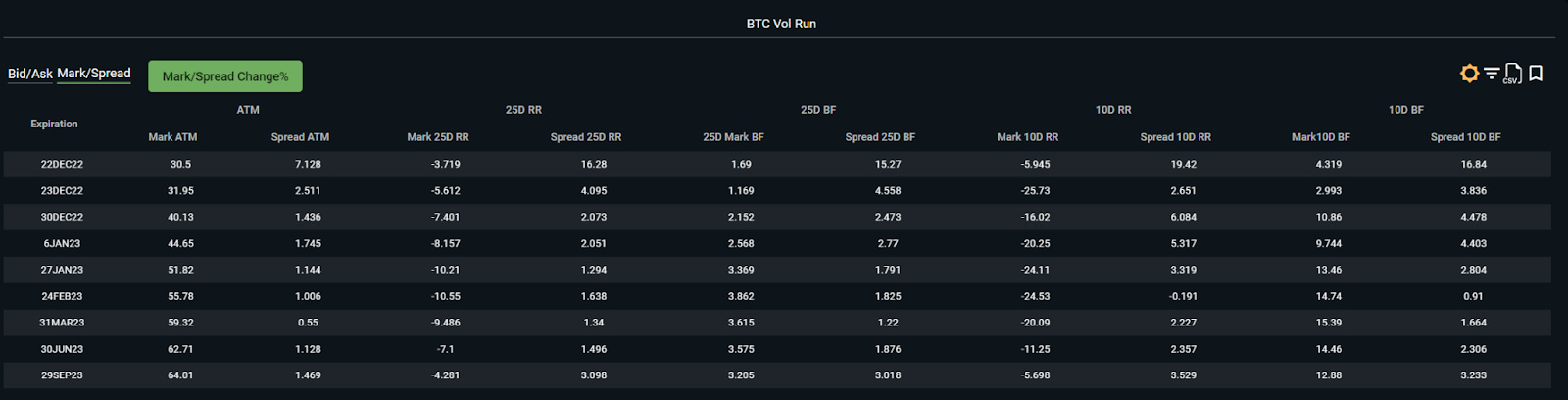

Vol Runs

Runs on both ETH and BTC post a near identical picture when looking at changes over 2ks with Riskies posting a decline (Put vol higher) and Flies showing increased convexity. As a Christmas bonus, readers will be pleased to find that you can now access Vol runs on Alt coins, in collaboration with OrBit Markets. These can be accessed under Options > Alt Coin. We will increase the number of assets accessible in due course and welcome feedback on any desired coins.