Coinvexity 15

With persistent inflation and a hawkish Fed, markets have yet to see some much needed relief.

Perpetuals - Global Market

BTC

ETH

Basis in BTC and ETH perps remain drawn to 0 with only OKX exhibiting marginally positive basis coupled with a clear shift downward in OI across all exchanges but FTX. APR across BTC is largely positive, in direct contrast to ETH whose values are mostly subdued as traders unwind ETH POW hedges post-merge.

Futures - Global Market

BTC

ETH

The standout feature here is the apparent bias of positive basis for OKX even as open interest continues to wane across the board.

Futures Basis Term Structure

BTC

ETH

Basis term structure in both BTC and ETH are diametric for the remainder of 2022 with FTX sitting at pole position in both instances. Interestingly BTC exhibits much tighter form with ETH showing greater dispersion.

Looking into 2023, ETH alludes to some form of reduced bleeding as basis trends less negative and levels begin to converge on 31/03.

Options

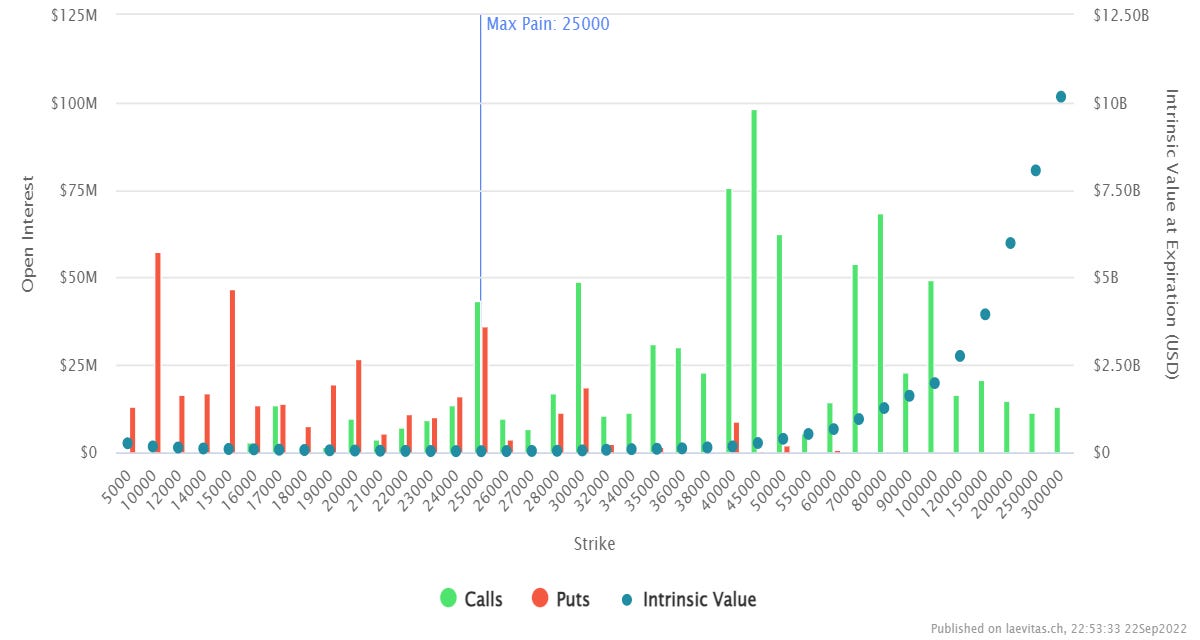

BTC Open Interest by Expiration

BTC Notional Open Interest 30 Sep

BTC Notional Open Interest 30 Dec

A quick glance in at options shows an anticipated and clear build up in quarterly expiries. The Sep expiry still exhibits heavy concentration <40k with close to USD 320mio in Calls alone between 24-35k. The Dec expiry has less focus in the 30s’ and is skewed more towards the upside (albeit with less overall volume) with USD +200mio between 40-50k and a further USD +150mio placed north of 70k.

1wk Implied Vol Spread

The 1wk IV spread space has been an interesting watch. With the ETH merge front and centre of everything crypto, near-end IV in ETH crept up to the point that it overtook SOL and pushed the SOL-ETH spread negative. We expect levels to soon normalise especially given that the ETH-BTC spread has halved from 40 to 20 in 2 weeks.

1mo Implied Vol

On the subject of expecting levels to normalise, 1mo vol in ETH entered June entangled with BTC while SOL remained aloft. Following late June’s shock, ETH tore itself from BTC and subsequently coupled with SOL. Now the merge flurry is done, perhaps there’s an opportunity to sell down ETH vol funded by a purchase in either counterpart as a hedge?

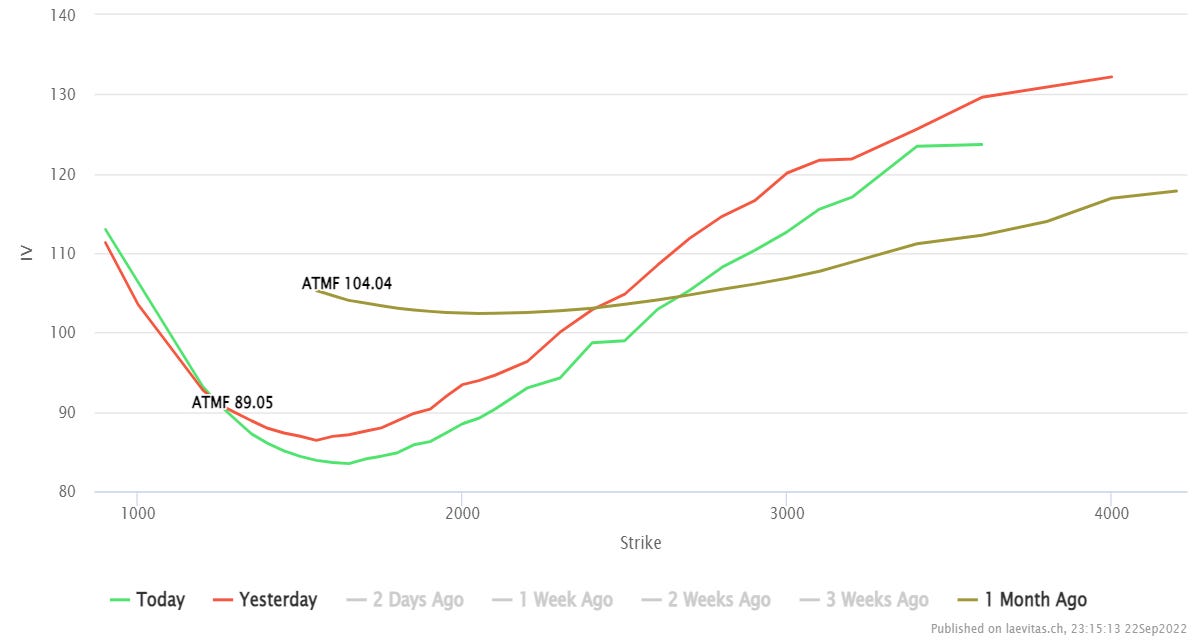

ETH Time Lapse ATM IV Term Structure

In keeping with the theme of ETH IV, we can clearly see the collapse in ATM IV as the curve was initially inverted in anticipation of mid September’s hoopla but has since seen IV washed out from +100 levels back down to mid/high 80’s.

ETH Skew Time Lapse 28 Oct Expiry

The same phenomenon is evident here as the smile has shifted lower, draining all of last month’s ATM impetus. Complementing this is the increased convexity (on a fixed strike basis) as OTM vol picks up along the wings. Further we see a small tilt in the o/n surface as downside IV increases marginally.

With IV dropping in ETH and vol spreads at a point of inflection, this might be an opportunistic moment to take advantage of our latest offering Exotic offering in conjunction with OrBit Markets, the Digital Option.

For a premium, a digital option allows/obliges you to pay/rcv a fixed notional amount if the spot rate fixes beyond a predetermined level. Our pricing grid allows you to quickly glance at an array of tenors and payouts, and should you wish to execute a trade you will be able to do so by clicking through the icon in the top right corner.